INTRODUCTION

The dental implant market world is shifting. While markets in North America and Western Europe are getting crowded, medical device companies are turning their attention to the fast-growing Asia-Pacific (APAC) region. In this mix, India isn’t just a “maybe”—it is becoming a major player that will likely change how dental care is consumed in the region. This blog gives you a quick look at the Indian market, which is booming thanks to demographic, economic, and clinical factors.

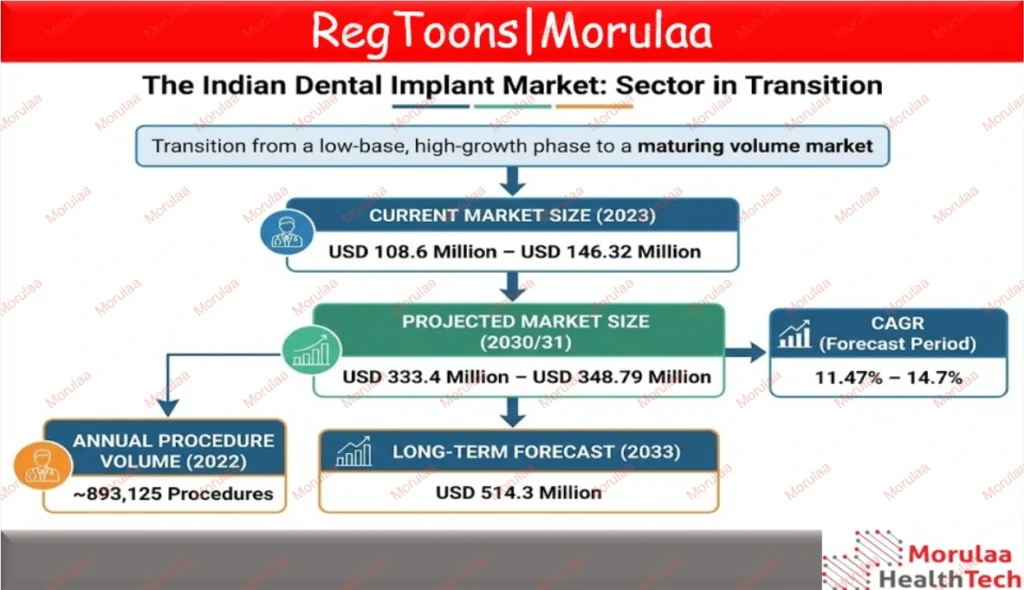

India has always been price-conscious, but the market is quickly focusing on quality. This change is happening because there are more older people needing tooth replacement, a growing urban middle class with money to spend, and a strong dental tourism industry bringing in international patients who want affordable care. We expect the market to hit between USD 333.4 million and USD 514.3 million over the next decade, growing much faster than the global average. However, getting in isn’t easy. The biggest hurdle is the strict rules enforced by the Central Drugs Standard Control Organization (CDSCO).

Under the Medical Device Rules (2017), dental implants are now classified as moderate-to-high risk (Class C) devices. This means you need a serious compliance strategy that matches global standards like the EU MDR and U.S. FDA. This report gives international manufacturers a practical guide to entering India and explains why it is vital to keep your regulatory license separate from your sales network. Working with specialists like Morulaa HealthTech lets manufacturers hold onto their regulatory control while keeping the freedom to choose different distributors. By breaking down market segments, competitor moves, and the paperwork involved, this document acts as your playbook for successfully growing in India.

WHAT IS DRIVING THE MARKET?

The Aging Population

The biggest driver here is simple demographics. India is famous for its young workforce, but we often overlook that it is also home to one of the world’s largest aging populations. The 60+ age group is growing fast. Unlike their parents, who might have just accepted losing teeth or wearing loose dentures, today’s seniors are more informed and have the savings to pay for better solutions.

Gum disease and cavities are still common issues across the country. Since people are living longer, they need their teeth to work for longer, making restoration critical. We are also seeing a clear move away from removable dentures toward fixed implants. This isn’t just about comfort—it’s also driven by the popularity of “teeth in a day” treatments promoted by big dental chains.

Dental Tourism in India

India has become a major destination for medical travel, which is a huge win for the premium implant market. The Price Advantage: A single implant in the US or UK can cost $3,000 to $5,000. In India, patients get the exact same top-tier brands (like Nobel Biocare or Straumann) for just $600 to $1,000. Better Clinics for Everyone: This flow of international patients has pushed Indian clinics to level up—adopting better technology (like 3D scans) and stricter hygiene standards. This ultimately raises the quality of care for local patients too.

Aesthetic Consciousness in the Post-Pandemic Era

Since the pandemic, people care much more about how their smiles look. With the rise of video calls, people became hyper-aware of their appearance, sparking a demand for cosmetic dentistry to boost confidence. Younger Patients: While older patients mostly care about function (chewing), younger people are driving the demand for single-tooth replacements, usually to fix a visible gap in the front after an accident or a missing tooth at birth. Metal-Free Options: This younger group is also pushing the trend for Zirconia (ceramic) implants, which they view as a more natural, holistic alternative to titanium.

MARKET ARCHITECTURE AND QUANTITATIVE ANALYSIS

The data shows a market in transition. It is moving from a “small but fast” startup phase into a serious, high-volume industry. There is a clear gap between how much money is being made (revenue) and how many products are actually being sold. While the sheer number of implants used is skyrocketing, growing about 15-18% every year, the price per unit is staying flat or even dropping. This is largely because affordable Korean and Israeli brands are flooding the market and driving prices down. Future growth isn’t going to come from raising prices; it will come from selling more units.

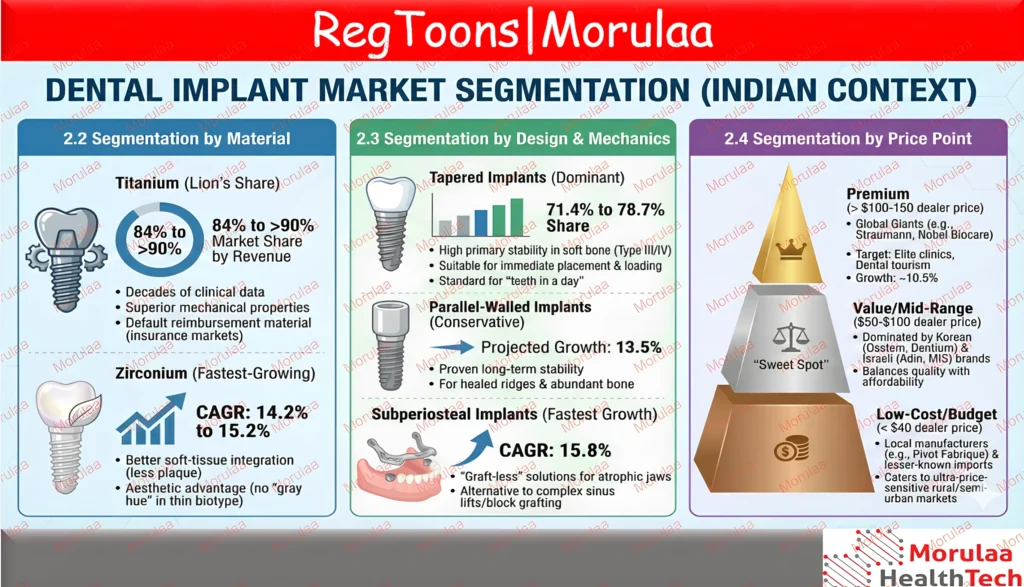

The dental implant market industry is shifting toward aesthetic precision and faster clinical outcomes. Titanium remains the industry gold standard with a 90% share due to its proven durability, while Zirconia is the fastest-growing segment for patients seeking metal-free, holistic solutions and superior “smile zone” aesthetics.

Clinically, Tapered implants dominate (~75% share) as their design provides the high primary stability essential for “Same-Day Teeth” (Immediate Loading). For complex cases involving significant bone loss, modern Subperiosteal designs offer a specialized, graft-less alternative to invasive surgery.

The market follows a clear tier system. Premium brands (e.g., Straumann, Nobel Biocare) lead in Swiss/American engineering and clinical research for complex cases. Meanwhile, the Value segment represents the market’s “sweet spot,” providing high-quality, clinically proven technology that balances advanced performance with broader accessibility.

The dental implant market industry is shifting toward aesthetic precision and faster clinical outcomes. Titanium remains the industry gold standard with a 90% share due to its proven durability, while Zirconia is the fastest-growing segment for patients seeking metal-free, holistic solutions and superior “smile zone” aesthetics.

Clinically, Tapered implants dominate (~75% share) as their design provides the high primary stability essential for “Same-Day Teeth” (Immediate Loading). For complex cases involving significant bone loss, modern Subperiosteal designs offer a specialized, graft-less alternative to invasive surgery.

The market follows a clear tier system. Premium brands (e.g., Straumann, Nobel Biocare) lead in Swiss/American engineering and clinical research for complex cases. Meanwhile, the Value segment represents the market’s “sweet spot,” providing high-quality, clinically proven technology that balances advanced performance with broader accessibility.

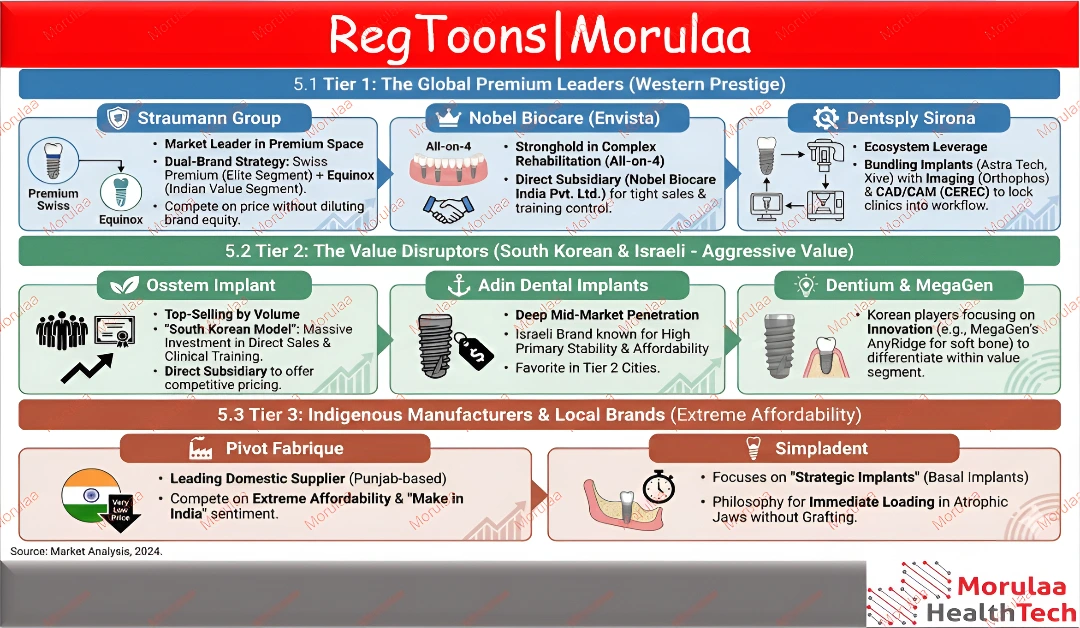

The global dental implant market competitive landscape is a strategic balance between premium prestige and value-driven innovation. Tier 1 is led by industry giants like Straumann, Nobel Biocare (Envista), and Dentsply Sirona, who dominate through advanced digital workflows, dual-brand strategies, and specialized solutions for complex rehabilitations.

Complementing these are value disruptors such as Osstem, Adin, and Dentium, which drive significant market volume by offering high-quality, clinically proven technology at accessible price points. From Swiss-engineered premium systems to local indigenous manufacturers like Pivot Fabrique, the market’s tiered structure ensures a versatile range of solutions that cater to both elite clinical demands and high-volume patient needs.

DENTIST DEMOGRAPHICS AND THE "TRAINING GAP"

India has a massive number of dentists, but turning them into dental implant market experts is harder than it looks. As of 2025, the Dental Council of India lists roughly 378,489 registered dentists. However, most of these professionals are packed into the big Tier 1 cities. While the total numbers look huge, the distribution is uneven, and many areas still fall short of WHO recommendations.

The bigger issue is the training itself. Dental school in India is great for theory but weak on hands-on practice. While about 75% of students learn the concepts of implants, only about 12% actually get to place one before they graduate. Because universities aren’t filling this gap, private training courses are booming. Companies that step in to teach these skills like Osstem or Nobel Biocare win big. They build loyalty with dentists early in their careers simply by being the ones to show them the ropes.

The market is heavily influenced by Key Opinion Leaders who run training academies and high-volume clinics. Notable names identified in the research include:

- Dr. Gunaseelan Rajan (Chennai): A pioneer in Zygomatic implants and medical director of Rajan Dental Hospital.

- Dr. Dilipkumar (Chennai): A veteran with over 20 years of experience.

- Dr. Rajesh Kumar Gupta: Recognized for implantology leadership.

- Dr. Prem Alex Lawrence: Known for “Full Arch in a Day” procedures.

- FMS Dental Hospital (Hyderabad): A key institutional player, placing over 25,000 implants with a team of maxillofacial surgeons.

- jaws without grafting.

India’s geography calls for a strong, multi-tiered distribution network. Unlike smaller countries where a direct-sales approach may be effective, the Indian market depends on a network of regional distributors to ensure reach, reliability, and sustained market penetration.

Key Distributors: Research identifies major regional players such as Vasant Distributors, Dental Concepts, Confident Dental, and Unicorn Denmart. These entities often hold exclusive rights for specific regions or brands. Price Discovery: The market is transparent yet varied. Listings show implants ranging from INR 750 (generic/local) to INR 4200+ (branded value) and up to INR 25,000+ (premium), illustrating the massive price disparity.

REGULATORY ENVIRONMENT (CDSCO)

Entering the Indian dental market now requires a more structured and regulated approach, Under the Medical Device Rules (MDR 2017), dental implants including fixtures, transgingival, and transmandibular types are strictly regulated as Class C (Moderate-to-High Risk) devices. This classification shifts the oversight from state authorities to the Central Licensing Authority (DCGI) in Delhi, necessitating a rigorous burden of proof for biocompatibility (ISO 10993) and clinical safety.

The registration roadmap begins with the appointment of an Indian Authorized Agent (IAA). As the license holder, your IAA manages the technical dossier via the SUGAM portal. While the general process for Form MD-14 import licenses is standardized, dental dossiers require specific technical granularity: manufacturers must provide detailed sterilization validation (Gamma/EtO), material specifications for Titanium Grade 4/5, and a valid Free Sale Certificate (FSC) from a GHTF country to streamline local clinical requirements.

THE "DEVICE FAMILY" PITFALL: A $7,500 LESSON

The most common financial oversight for dental manufacturers lies in the definition of a “Distinct Device Family.” While a manufacturer might view their entire portfolio as a single range of titanium implants, the Central Drugs Standard Control Organization (CDSCO) applies a stricter clinical lens.

For instance, a European manufacturer recently attempted to bundle Tapered, Zygomatic, and One-piece implants under a single $1,500 family fee. The Central Drugs Standard Control Organization (CDSCO) rejected this, ruling that the variations in anatomical site (posterior maxilla vs. alveolar ridge) and surgical technique necessitated three separate applications. This shifted their government fee from an expected $4,500 to **$7,500** (including the $3,000 site fee).

The Takeaway: To avoid unexpected costs and the common 9–12 month timeline extensions caused by technical queries (RFIs), manufacturers must align their “Device Family” strategy with the Central Drugs Standard Control Organization (CDSCO’s) clinical consistency standards before submission.

STRATEGIC MARKET ACCESS: THE INDEPENDENT AGENT ADVANTAGE

A critical, often overlooked strategic decision is who holds the Import License (MD-15). Many manufacturers simplify entry by appointing their commercial distributor as their Authorized Agent. However, this creates a “regulatory hostage” risk: if the commercial partnership fails, the license remains with the distributor, often forcing the manufacturer to restart the months-long registration process from scratch.

The Morulaa Solution addresses this by acting as an Authorized Agent. By separating regulatory compliance from commercial distribution, Morulaa holds the MD-15 and manages the import logistics without engaging in end-user sales. This model ensures the manufacturer retains absolute ownership of their market access. You gain the flexibility to hire, fire, or expand your distributor network at will, ensuring that your regulatory status remains stable even if your commercial strategy evolves.

Beyond the License: Operationalizing Your Supply Chain

For dental manufacturers, the challenge shifts from regulatory approval to logistical execution. With hundreds of SKUs across varying implant lengths and diameters, a fragmented supply chain is a significant risk.

Morulaa’s 4PL (Fourth-Party Logistics) model streamlines this by managing the “last mile” of compliance. We handle the Bill of Entry (BOE) and ADC clearances at the port, ensuring immediate No Objection Certificates (NOC) to prevent costly customs delays. Crucially, we manage Compliance Labeling (MRP and Importer details) and provide Sterility-Validated Warehousing before products are dispatched to your local partners. This ensures your high-value inventory remains compliant and market-ready from the moment it lands in India.

Data-Driven Distributor Strategy

In India’s federal market, the “right” distributor is rarely found on a generic list. Success requires a bifurcated strategy: balancing national reach with regional exclusivity. Morulaa leverages a proprietary database of 500+ vetted partners to move beyond simple introductions. We conduct a rigorous SWOT analysis and financial vetting of potential distributors, assisting you in contract negotiations to ensure your commercial terms are as robust as your regulatory ones.

Leveraging Global Compliance: EU MDR & US FDA

While the target is India, your success relies on the strength of your global technical dossier. The transition to EU MDR (2017/745) and the rigors of US FDA Vigilance are now the foundational pillars for Indian Class C approvals.

The EU MDR Bridge: For dental implants (Class IIb/III), we support the transition from old MDD files to the new MDR structure. This includes the development of Clinical Evaluation Reports (CER) , a living document under MEDDEV 2.7/1 and the management of annual Periodic Safety Update Reports (PSUR).

The FDA Vigilance Shield: In a high-volume reporting environment like the FDA MAUDE database, managing osseointegration or fracture reports is critical. Morulaa provides Complaint Triage, helping you distinguish between reportable malfunctions and use errors. We manage the technical execution of eSubmitter/eMDR filings, ensuring your global standing remains pristine.

Check out our blog to learn more for ” Navigating India’s Medical Device Market: Key Insights for Global Manufacturers”

CONCLUSION

The Indian dental implant market offers unparalleled volume potential, but the era of unregulated, “trial-and-error” entry is over. With the Central Drugs Standard Control Organization (CDSCO’s) Class C requirements now firmly in place, success depends on a unified strategy that bridges high-level global compliance with localized, independent market access. By separating your regulatory identity from your commercial distributors, you ensure that your growth in India is not just rapid, but sustainable.